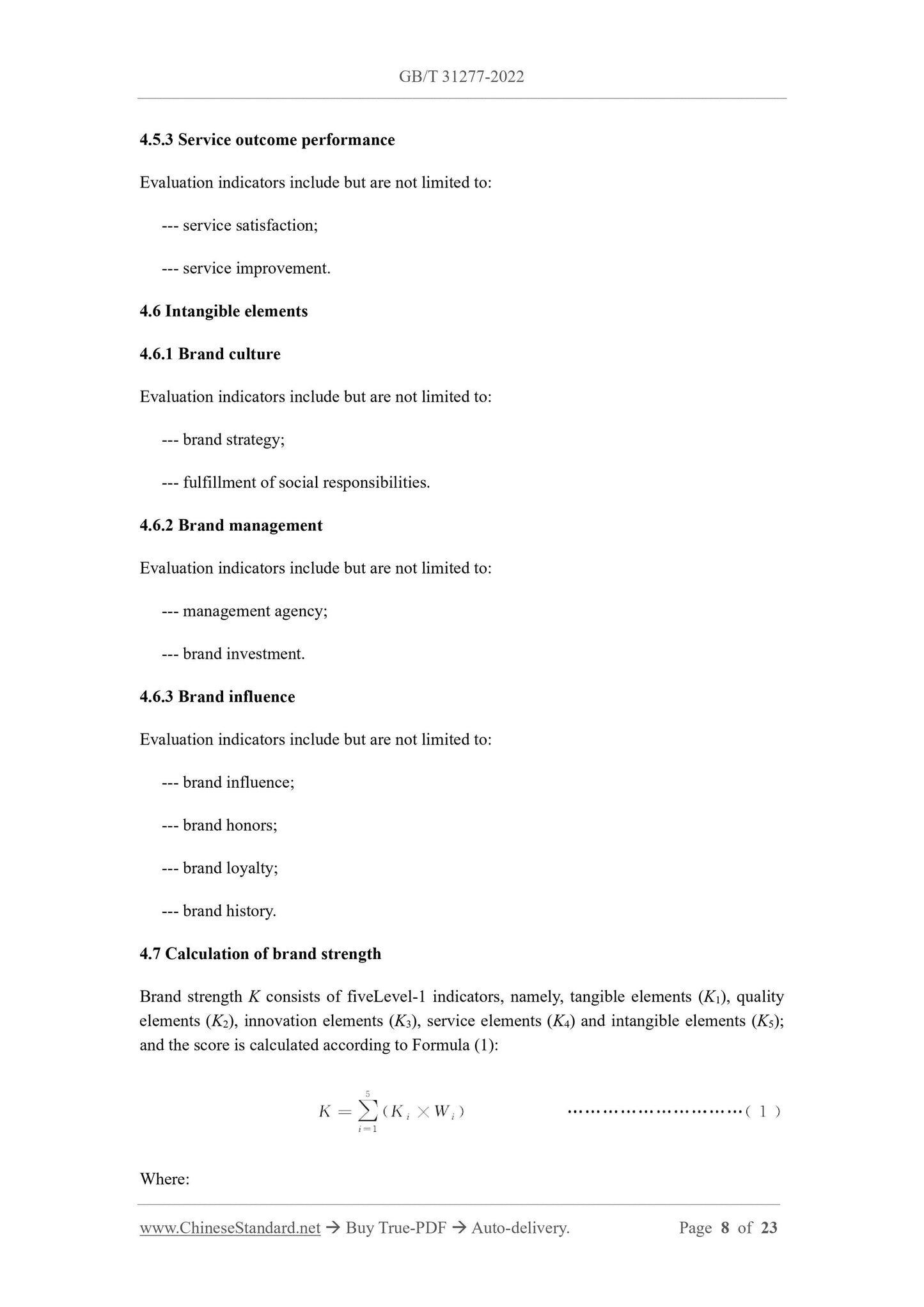

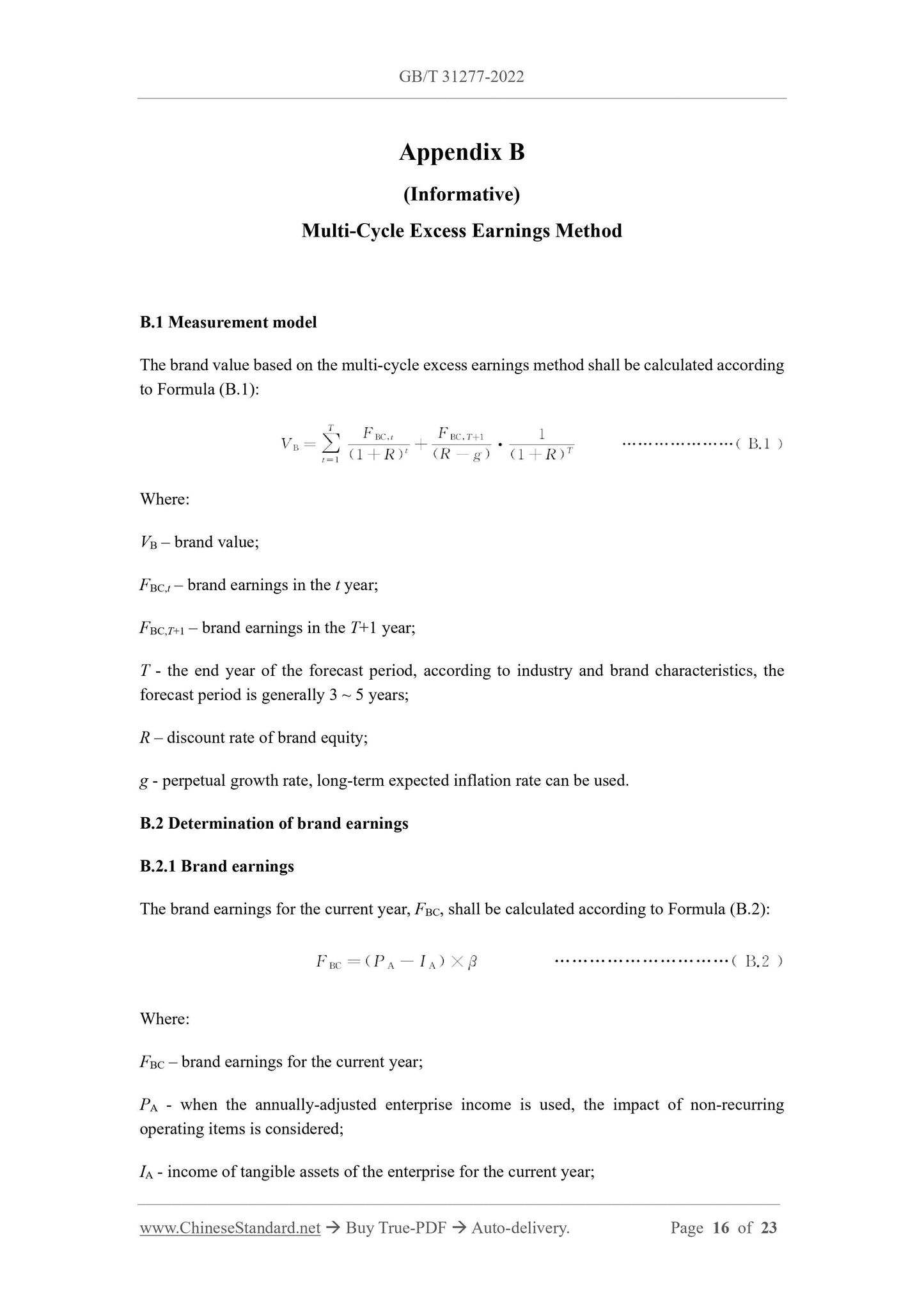

This Document specifies the brand strength, measurement model, and evaluation process for brand valuation in the retail industry. This Document is suitable for brand valuation of retail enterprises, and can be used for self- evaluation or third-party evaluation.

Basic Data

Standard ID

GB/T 31277-2022 (GB/T31277-2022)

Description (Translated English)

Brand valuation - Retail industry

Sector / Industry

National Standard (Recommended)

Classification of Chinese Standard

A00

Word Count Estimation

17,129

Issuing agency(ies)

State Administration for Market Regulation, China National Standardization Administration